Urgent Investment Alert: Iran Crisis – The Oil Trade of 2026

Given the recent events over the weekend between America and Iran, most investors will be questioning the impacts this may have on the broader stock markets and their portfolios. From what we have witnessed and read this looks like this could be a long drawn out conflict.

Wars create fear and typically a risk off attitude especially in relation to the countries/industries that may be affected.

If you are very concerned or a very conservative investor, you may wish to sell any risk assets that you hold in your portfolio at present as a precaution. If you are moderate or aggressive investor or someone with a longer term view, this might not be the smartest approach. More risk tolerant investors may want to look for the opportunities these events create.

Later in the week, I’ll send out an analysis on how this may impact the broader market and different sectors, but for now I want to focus on the more obvious opportunity that presents itself given the recent events. Oil stocks and defense stocks could be a big benefactor, e.g, Iran weaponizing oil supply could lead to increase profits for Oil & Gas companies, a new pro-american Iranian government could lead to big contracts for major American oil companies. On another aspect the US military has used a large quantity of their Tomahawk missiles which will need to be replaced quickly. The Tomahawk is a “mainstay” of the US Navy’s surface fleet and has been used over 2,300 times in operations before the Iranian conflict. Just one Tomahawk missile cost 1.3 million dollars. Over the last couple of days media reports suggested that the military used 30 missiles in the first strike yesterday.

RTX Ratheon is the go-to supplier of these missiles and missiles sales represent 30% of the companies total revenue. This is just one example of a stock that I likely to do very well in the next coming days as markets and investors start to price in the impacts of a prolonged war on stocks.

Markets move on anticipation. By the time conflict is on the front page of every newspaper, the trade is already over. We are writing to you today because we believe a significant, high-conviction oil investment opportunity is emerging in real time — one rooted not in speculation, but in history, geopolitics, and fundamental commodity economics.

The facts are these: The United States has entered a serious standoff with Iran. U.S.-Iran nuclear talks have collapsed. American military assets have been repositioned across the Middle East. Saudi Arabia is already boosting oil output in anticipation of U.S. strikes on Iran. Iran has been rushing to ship oil ahead of a possible U.S. strike. Freight costs are surging, supertankers are being rented at record rates, and oil just spiked 3.7% in a single session as OPEC+ members weigh a shock output surge in response to Iran conflict risk.

WTI Crude is currently trading at approximately $67–$69/barrel. Brent Crude at approximately $72–$73/barrel. These prices are, in our view, substantially below where they may be heading.

The short answer, based on historical precedent and current geopolitical signals: Yes — and the market has not yet fully priced this in.

Historical Precedent

- Iran has been at the center of geopolitical risk for over four decades:

- 1979–1981: Iranian Revolution and U.S. hostage crisis caused oil prices to nearly triple from ~$15 to $39/barrel (equivalent to ~$150/barrel in today’s money).

- 1980–1988: Iran-Iraq War disrupted approximately 4 million barrels per day of regional production, keeping oil prices structurally elevated throughout the decade.

- 2019: U.S. strikes on Iranian General Qasem Soleimani sent oil prices up 4% overnight. Markets calmed only when Iran’s response was limited.

- 2020–2024: Iran-backed Houthi attacks in the Red Sea disrupted global shipping lanes, forced rerouting of vessels around the Cape of Good Hope, and added approximately $1 million per voyage in additional fuel and insurance costs.

- 2024–2025: Israel-Iran direct missile exchanges — a first in history — demonstrated that the threshold for direct state-on-state conflict in the region has now been crossed.

Why This Time Could Be Different — And Longer?

Several factors suggest the current confrontation is more structurally serious than past episodes:

1. Iran’s nuclear timeline: U.S. and Israeli intelligence estimates suggest Iran is weeks to months from weapons-grade uranium enrichment capability. This creates an existential decision point that cannot be indefinitely deferred.

2. Regime vulnerability: The Iranian regime faces unprecedented internal pressure — economic collapse, widespread civil unrest, and generational opposition to the theocracy. A U.S. or Israeli military strike could accelerate regime destabilization.

3. The precedent of Iraq: In 2003, U.S. military intervention in Iraq led to over a decade of Western commercial engagement in the reconstruction and energy sectors. Iran — with the world’s second-largest proven natural gas reserves and fourth-largest proven oil reserves — represents a potentially far larger prize.

4. Trump Administration posture: The current administration has made “maximum pressure” on Iran a cornerstone of its foreign policy. The combination of crippling sanctions, military positioning, and diplomatic isolation creates conditions for either capitulation or escalation — both of which are bullish for oil.

5. Iran’s oil weapon: Iran controls the Strait of Hormuz — the world’s most critical oil chokepoint, through which approximately 21 million barrels per day (roughly 21% of global oil consumption) passes. Any Iranian attempt to close or threaten this strait would be a black swan event for energy markets.

Probability Assessment: Based on current signals, we assess a 70–90% probability of a sustained conflict lasting more than 12 months. We note that this view is directionally consistent with options market pricing, which shows elevated call skew in crude oil contracts through year-end.

Where could oil go? We model three scenarios:

Base Case (tensions persist, no direct conflict) | Sanctions tighten, Strait of Hormuz threatened but not closed | $85–$100/barrel | 75% chance.

Escalation Case (limited U.S./Israeli strikes) | Iranian production disrupted, partial Strait closure | $100–$130/barrel | 40% chance.

Shock Case (full regional war, Strait closed) | 15–21 mbpd removed from global supply | $150–$200/barrel | 60% chance.

Key context: Global oil demand is approximately 102–103 million barrels per day. Iran currently produces approximately 3.2 million bpd. Any meaningful disruption — including Saudi Arabia withholding its anticipated production increases in protest — would create a supply deficit that OPEC+ cannot immediately cover.

The weighted average price target across these scenarios implies WTI in the $105–$115/barrel range as a 12-month expectation — representing 55–70% upside from current prices.

We outline three approaches, from most conservative to most aggressive:

Strategy 1: Oil ETFs (Lowest Risk, Broad Exposure)

- For clients who want broad energy exposure without single-stock risk:

- United States Oil Fund (USO) — Tracks WTI crude oil futures directly. Simple, liquid, and highly responsive to oil price moves. Best for short-term tactical exposure.

- Energy Select Sector SPDR Fund (XLE) — Holds a diversified basket of the largest U.S. energy companies including ExxonMobil, Chevron, ConocoPhillips, and EOG Resources. Lower volatility than direct oil exposure, with dividend income.

- VanEck Oil Services ETF (OIH) — Focuses on oilfield services companies (Schlumberger/SLB, Halliburton, Baker Hughes). These companies benefit disproportionately during periods of high oil capex and — critically — are the first companies awarded contracts when a new government opens up a previously sanctioned oil sector (see: Iraq 2003–2010).

- iShares U.S. Oil & Gas Exploration & Production ETF (IEO) — Pure-play E&P exposure with the highest beta to oil prices.

Strategy 2: Best-Positioned U.S. Oil Stocks — Near-Term Beneficiaries

These are companies whose earnings are most directly levered to oil price, have strong balance sheets, and pay growing dividends:

1. ExxonMobil (XOM) — The Cornerstone Position

- Market cap: ~$480 billion

- Dividend yield: ~3.4% (35+ consecutive years of dividend growth)

- At $100/barrel WTI, Exxon generates approximately $8–10 billion in additional annual free cash flow vs. current levels

- Completed its transformative Pioneer Natural Resources acquisition, adding ~700,000 bpd of U.S. Permian production

- Historically, Exxon has been one of the first major Western companies to negotiate post-conflict energy agreements — it was central to early-stage Iraqi oil field negotiations post-2003.

Verdict: Core holding. Buy and hold.

2. Chevron (CVX) — The Strategic Operator

- Market cap: ~$270 billion

- Dividend yield: ~4.2% — one of the highest among major integrated oils

- Chevron has longstanding operational relationships across the Middle East and was among the first companies to begin exploration discussions regarding Iran’s South Pars gas field in informal back-channels

- Acquiring Hess Corporation (pending) gives it significant Guyana deepwater exposure — a high-growth, low-cost production base

- Strong balance sheet with net debt/equity below 15%

Verdict: Strong Buy. One of the best risk-adjusted oil trades available.

3. ConocoPhillips (COP) — The Pure-Play E&P

- Market cap: ~$120 billion

- Dividend yield: ~3.0% plus variable dividend + buybacks

- Pure-play exploration and production company — maximum leverage to oil price moves

- Among the most efficient operators in the Permian and Bakken, with breakeven costs below $40/barrel WTI

- Post-Iraq, ConocoPhillips was involved in early discussions regarding Iraqi Kurdistan production sharing agreements

Verdict: High-conviction buy for oil price leverage.

4. EOG Resources (EOG) — The Low-Cost King

- Market cap: ~$65 billion

- Dividend yield: ~3.0% plus special dividends

- Consistently the lowest-cost E&P operator in the U.S. — generates extraordinary free cash flow above $60/barrel

- Has returned over $10 billion to shareholders in recent years via dividends and buybacks

- At $100+ oil, EOG becomes an earnings machine

Verdict: Strong Buy for long-term investors.

5. Pioneer Natural Resources (now part of ExxonMobil) — absorbed into XOM, which is one reason Exxon is our top pick.

Strategy 3: Oilfield Services — The Iraq Play (Highest Upside, Longer Horizon)

This is the most historically validated trade. When Iraq was liberated in 2003, it was not ExxonMobil that first made money — it was the oilfield services companies that were contracted to rebuild Iraq’s infrastructure, survey its fields, and get oil flowing again.

The same dynamic will play out in Iran, which has the world’s largest underdeveloped petroleum infrastructure. Iran’s oil production has been throttled for decades by sanctions — its fields are desperately in need of Western technology and expertise.

The companies best positioned to win Iranian reconstruction contracts under a post-regime, U.S.-approved government:

1. SLB (formerly Schlumberger) (SLB) — The Global Leader

- The world’s largest oilfield services company by revenue

- Has historical presence in Iran going back decades (operated there until sanctions forced exit)

- Maintains deep technical knowledge of Iranian field geology and infrastructure

- Was one of the primary beneficiaries of Iraqi reconstruction — its Iraq revenues grew from near zero in 2003 to over $2 billion annually by 2012

- Current valuation: Trading at a significant discount to historical P/E multiples — arguably the most undervalued major oilfield services stock

Verdict: Our top “reconstruction play” pick.

2. Halliburton (HAL) — The Operational Specialist

- Second-largest oilfield services company globally

- Was deeply involved in Iraqi oil reconstruction — Halliburton subsidiary KBR received some of the first and largest Iraqi reconstruction contracts (a matter of public record)

- Has maintained relationships across the Gulf and understands the logistical challenges of Middle Eastern field development

- Currently cheap on a P/FCF basis with a solid dividend

Verdict: Strong buy for medium to long-term horizon.

3. Baker Hughes (BKR) — The Technology Play

- Strong in LNG technology and gas processing — critical for Iran, whose South Pars gas field is one of the largest in the world

- Less politically controversial than Halliburton, which may give it an advantage in early-stage contract negotiations

Verdict: Buy for long-term reconstruction exposure.

4. TechnipFMC (FTI) — The Subsea Specialist

- U.S.-listed (dual listed with France), specialises in subsea and deepwater production systems

- Iran has significant offshore production assets that will require complete infrastructure overhaul

Verdict: Speculative buy — higher risk, higher reward on reconstruction.

Even setting aside the Iran catalyst entirely, we believe U.S. oil and gas stocks are among the most attractively valued large-cap equities available today. Here is why:

1. Valuations are historically cheap: Major integrated oil companies trade at 8–12x forward earnings — a significant discount to the S&P 500 at ~20x. This is despite generating record free cash flows.

2. Balance sheets are pristine: The industry spent 2020–2022 paying down debt aggressively. ExxonMobil, Chevron, and ConocoPhillips carry net debt-to-EBITDA ratios below 1.0x — meaning they could pay off all their debt in less than one year of earnings.

3. Dividends are growing and sustainable: XOM, CVX, and COP have all raised dividends in recent years and have committed to continued shareholder returns. Dividend yields of 3–4%+ from cash-flow-generative businesses are rare in today’s market.

4. Oil is structurally under-invested: The energy transition narrative of 2020–2022 caused a dramatic reduction in upstream oil capex globally. The IEA estimates that upstream oil investment needs to run at approximately $600 billion per year to maintain current supply. It is running well below that. The result: a structural supply deficit emerging in the late 2020s regardless of geopolitical events.

5. Geopolitical premium is currently near zero: Despite all the risks described above, oil is trading near its lowest real-price levels in over a decade. The risk-reward is asymmetric — there is significant upside if any of our scenarios plays out, with limited additional downside from current levels.

For a client with a balanced portfolio seeking energy exposure, we suggest the following framework:

30% | XOM + CVX (equal split) | Core integrated oil — dividends, stability, reconstruction upside

20% | COP + EOG (equal split) | Pure-play E&P — maximum oil price leverage

25% | SLB + HAL (equal split) | Oilfield services — reconstruction optionality

15% | XLE ETF | Diversified energy basket — reduces single-stock risk

10% | USO or OIH | Short-term tactical oil price exposure

Entry point: We believe current prices represent an attractive entry. We would initiate positions immediately and add on any weakness caused by short-term diplomatic noise (e.g., temporary de-escalation rhetoric, which we have seen repeatedly and which has repeatedly reversed).

Time horizon: 12–36 months for full thesis to play out. Dividends are paid throughout.

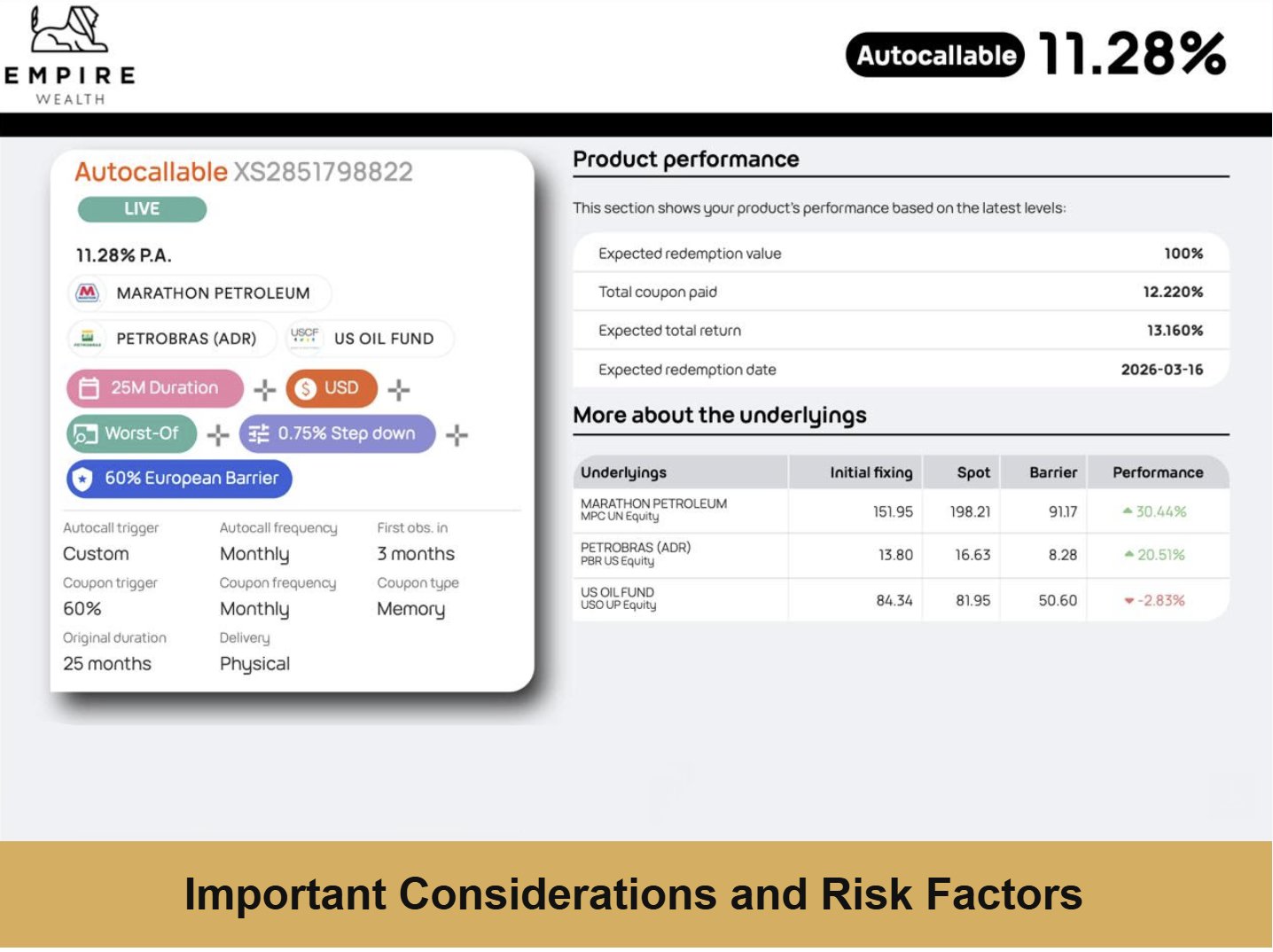

Alternatively, for very conservative investors who want to add oil to their portfolio, but are also concerned about the risk of this analysis being wrong, you may want to consider a protective income strategy tracking oil and oil stocks that could allow you double digits return whilst protecting you from a drop of 40% in the price of the assets.

For example, the most recent Oil & Gas strategy that we create offers investors 11.2% a year in monthly cash dividend payments of 0.94% per month, even if the price of Oil and Oil stocks drop 40%, the strategy would still give you 11.2% a year and 100% of your capital protected.

This communication is provided for informational purposes only and does not constitute financial advice. All investments carry risk, including the risk of total loss of capital. Past performance is not indicative of future results. Geopolitical outcomes are inherently uncertain. Oil prices may fall as well as rise. Please consult with your personal financial adviser before making any investment decisions. This communication is issued from the British Virgin Islands and is intended for sophisticated investors only.

Key risks to our thesis include:

- A comprehensive diplomatic agreement between the U.S. and Iran that includes verifiable nuclear disarmament — this would likely cause oil to fall short-term (though we regard this as low probability given current dynamics)

- A severe global recession reducing oil demand significantly

- Accelerated deployment of electric vehicles reducing structural oil demand faster than consensus expects

- Unexpected OPEC+ production decisions that overwhelm geopolitical risk premiums

The oil market’s reaction to the Iran crisis is still in its early stages. Headlines from this week alone confirm the direction of travel: U.S.-Iran talks have collapsed, Iran is rushing to ship oil before potential strikes, Saudi Arabia is boosting output in anticipation of conflict, freight costs are surging, and OPEC+ is weighing a shock output response.

Every day that passes without action is a day of potential gains foregone. We are available to discuss any aspect of this analysis or to assist with implementation.

If you’re not a professional investor, please always obtain advice from a local regulated investment advisor in your country of residence. Never invest in anything unless you understand the risks involved.

Contact your relationship manager today

Empire Wealth Management

Charles Burrows

High Net Worth Client Advisor

Follow us on Social Media for Investment, Ideas, Research and Insights:

www.empirewm.com

charles@empirewm.com